Is It Prudent to Invest in Bitcoin?

Is Bitcoin a prudent addition to investment portfolios? This blog explores historical data and considers the implications for risk, return, and diversification.

Authors: Andrew Bailey, Bradley Rettler and Craig Warmke

It is obvious to some people that no one should invest any of their assets into Bitcoin and other cryptocurrencies. It is obvious to some people that investors should put much if not all of their assets into Bitcoin and other cryptocurrencies.

How to decide? While past performance is no guarantee of future performance, it can be illuminating to see how an investment would have worked out in the past. If an investment had poor performance in the past, it is important to think about why the future may be different. If an investment had excellent performance in the past, it is worth thinking about whether those conditions may continue in the future.

A common refrain in financial literature is: diversify. Having all assets invested in one asset may work out well. Then again, maybe not. But sometimes it does.

Didi Taihuttu and his family sold all of their belongings in 2017 and bought bitcoin. That worked out well for them. When they were buying their initial stockpile, bitcoin was trading at around $900. Today, of course, bitcoin is around one hundred times that price. While Mr. Taihuttu has bought and sold cryptocurrencies in the meantime, he has done well, even starting his own Bitcoin Beach in Portugal for a while. (This apparently was abandoned when Portugal started taxing capital gains on cryptocurrencies.)

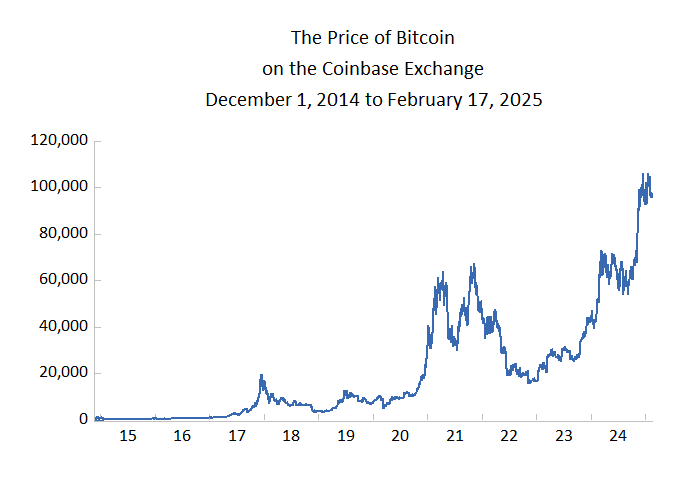

Going all in on cryptocurrencies could have worked out differently. As the attached figure shows, the overall trend of bitcoin is up. There have been brutal declines though. If Mr. Taihuttu had bought some bitcoin at its local peak of $67,510 per bitcoin on November 8, 2021, those bitcoin were worth just $15,756 a year later on November 21, 2022. Maybe he would have hung in there and continued holding it through its recovery and increase to subsequently higher values. Sad to say though, many investors have a hard time continuing an investment that has lost over 75 percent of its value. This is especially true if everything is invested in that asset.

While diversification makes the return of about 10,000 percent that Didi Taihuttu received from 2107 to 2025 very unlikely, diversification also makes the return of -75 percent in 2022 not very likely. Many people do not want to be a plunger like Didi Taihuttu. I consider the more common situation in which an investor trades off risk and return.

Common investments to consider are stocks and bonds. Gold is another possibility and bitcoin is yet another. Despite the common belief that bonds are low risk, Jeremy Siegel in Stocks for the Long Run shows that bonds can be quite risky due to inflation. To keep things simple, I consider a portfolio of all common stocks trading on U.S. exchanges and examine the effects on the portfolio's return of adding some bitcoin to it. Gold has had a lower average return and volatility than stocks. Bitcoin has had a higher average return and volatility than stocks. It is worthwhile to see the effect of bitcoin added to stocks by itself.

From 2015 to the end of 2024 when my data for common stocks end, the average annual return on all stocks in the United States is 11.4 percent per year. (This is measured by the Chicago Research in Securities Prices, CRSP, index.) The most common measure of volatility – the standard deviation – is 16.1 percent per year. This suggests that, in a typical year, an increase or decrease of 16.1 percent would happen about once every three years. For bitcoin, the average annual return over the same period is 75.5 percent per year and the standard deviation is 407 percent per year. The usual rules of thumb for the standard deviation cannot apply because a decrease of more than 100 percent is impossible. Still, there are two years when the price of bitcoin fell more than 60 percent. There also is one year – 2017 – when the price was 14 times higher at the end the year than at the start. Obviously big increases predominate since the price of bitcoin increased. All of that said, the volatility reflects the nontrivial probability of both big decreases and big increases.

Before proceeding, it is worth considering a common recommendation for a diversified portfolio: rebalancing it periodically. This advice holds especially for volatile assets such as bitcoin. A rebalanced portfolio is a portfolio that is managed to keep the fractions of the assets relatively constant. Consider a portfolio of two assets with a target of holding 50 percent of each. When one asset increases in value more than the other, then the fraction of that asset in the portfolio increases. Rebalancing the portfolio requires selling some of the asset that went up more and buying the other asset to return the portfolio to a 50-50 balance. It is not necessary to have a 50-50 allocation. The allocation could be much smaller for one asset than another.

The figure showing bitcoin's price suggests the usefulness of rebalancing for bitcoin. Precisely because bitcoin is very volatile, selling when the price has gone up and buying when the price has gone down can both keep the riskiness of the portfolio controlled and take advantage of that volatility to some extent. Rebalancing is a more mechanical version of the advice to "buy the dip." The investor lets the fraction of the portfolio in the assets tell him when to buy the dip, not intuition. A common rule of thumb is to rebalance periodically, quarterly or annually.

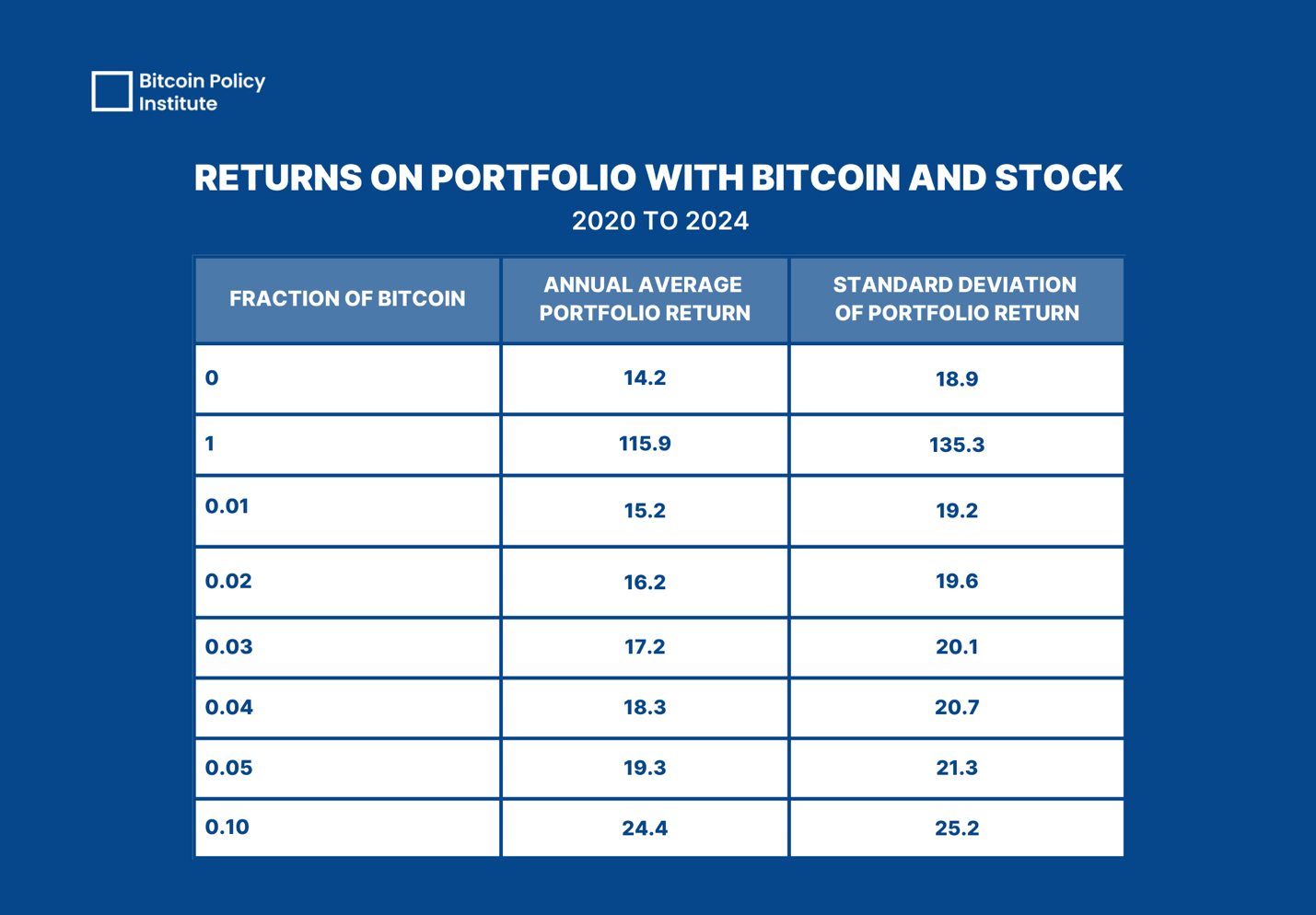

We can examine the implications of diversifying into bitcoin by examining the period 2020 to the end of 2024. The average annual return on corporate stock 14.2 percent per year and the standard deviation of that return is 18.9 percent per year. For bitcoin, the average annual return is 115.9 percent per year and the standard deviation is 135.3 percent per year. Obviously a portfolio of only bitcoin would have fared much better by the end of 2024 than a portfolio of stocks, but it would have been a bumpy ride indeed. That bumpy ride continues with bitcoin's price currently about $85 thousand, almost twenty percent below its peak in December 2024.

Using the data for 2020 to 2024, what would a portfolio of corporate stock and some bitcoin have returned? The table below shows the mean and standard deviation of a portfolio of stocks and bitcoin that are rebalanced once a year. While rebalancing more frequently might be better, these returns are intended to be illustrative, not predictive.

The table shows the fraction of bitcoin in the portfolio, the average annual return on the portfolio and the standard deviation of the return on the portfolio. For comparison purposes, portfolios with no bitcoin and only bitcoin are included with the fractions 0 and 1 of bitcoin in the portfolio.

Even a small amount of bitcoin can add materially to the portfolio's return. While an extra one percent per year may not seem like much, it adds over 10 percent to the portfolio's value after ten years. Holding only one percent of the portfolio in bitcoin would have made a big difference from 2020 to 2024. Adding bitcoin increases the return linearly, by about one percent per year extra return for each one percent extra of bitcoin held. The volatility, the standard deviation, though is increasing little at first and then more with larger fractions of bitcoin in the portfolio.

Past performance is no guarantee of future performance. Still, the data indicate that adding some bitcoin to a portfolio of common stocks can increase the return without unduly increasing the risk.