Letter to Congress in Support of De Minimis Exemptions for Bitcoin Payments

Congress should extend de minimis tax relief to both payment stablecoins and major network tokens like Bitcoin to make everyday digital asset payments practical.

Bitcoin Policy Institute

January 12, 2026

The Honorable Michael Crapo

Chairman, Committee on Finance

U.S. Senate

Washington, D.C. 20510

The Honorable Jason Smith

Chairman, Committee on Ways and Means

U.S. House of Representatives

Washington, D.C. 20515

Dear Chairman Crapo and Chairman Smith:

We, the undersigned organizations and companies, write to express our appreciation for both of your Committees' ongoing work to provide clear, durable rules for the taxation of digital assets and to comment on potential de minimis tax provisions for small digital asset transactions. We are concerned that current discussions may result in a de minimis exemption limited only to 'payment stablecoins' meeting the requirements laid out in the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, without extending comparable relief to Bitcoin and other network tokens that underpin those same payments.¹

We are also concerned that basing a de minimis threshold on capital gain or loss, rather than transaction value, would fail to achieve the intended simplification in calculation and reporting.

As Congress has recognized in recent bipartisan market structure proposals, digital assets serve distinct functional roles. These proposals distinguish payment stablecoins from network tokens - digital assets that are integral to the operation, security, and transaction execution of open blockchain networks and that are not issued or backed by a centralized entity.

The goal of the undersigned is to ensure that any de minimis regime reduces tax compliance burdens for ordinary users, small businesses and federal agencies, while aligning the treatment of widely used digital assets with existing small-transaction exemptions in the tax code. As merchant and consumer adoption of digital assets to purchase goods and services continues to grow, it is imperative that policy keeps pace so the U.S. can maintain leadership in digital assets and payments innovation.

Congress took an important step by enacting the GENIUS Act, establishing a federal framework for U.S. payment stablecoins so that they can scale safely and reinforce U.S. dollar leadership in global payments. As Congress considers accompanying tax legislation, it is essential to recognize that payment stablecoins do not operate in a vacuum; they run on open blockchain networks that rely on separate network tokens for consensus, security, and transaction execution. For that reason, we propose three main policy solutions for consideration:

- Apply cash-like treatment for GENIUS-compliant payment stablecoins.

- Ensure de minimis relief applies to network tokens, as defined under federal digital asset market structure frameworks.

- Adopt value-based accounting with reasonable per-transaction and annual caps.

De minimis exemptions in tax law and digital assets

De minimis provisions in the Internal Revenue Code exist to avoid imposing disproportionate reporting and recordkeeping burdens on taxpayers for very small or everyday transactions. For a decade, experts and lawmakers have proposed extending de minimis relief for digital assets like Bitcoin precisely because treating each small transaction as a taxable disposition is impractical when assets are used as a means of payment.

The urgency of getting de minimis policy right is heightened by the new broker reporting rules for digital assets. The Treasury and the IRS have finalized regulations implementing new requirements for brokers to report sales and certain exchanges of digital assets on new Form 1099-DA for transactions occurring on or after January 1, 2025.

While the IRS has provided transitional relief on certain penalties for 2025 as brokers implement the new rules, the direction is clear: billions of digital asset transactions will soon be reported on 1099-DA, and taxpayers will be expected to reconcile these forms on their returns.² Without calibrated de minimis relief, the result will be widespread discrepancies, unnecessary audit risk, and reporting complexity vastly disproportionate to the economic substance of the transactions involved. Even trivial on-chain network fees—often amounting to only a few cents—would generate complex taxable events for both brokers and taxpayers. A value-based threshold—paired with reasonable per-transaction and annual caps—better reflects how existing de minimis provisions operate for everyday consumer transactions and avoids imposing gain- or loss-based calculations that are ill-suited to high-volume, low-value activity on blockchain networks.

Core concern: de minimis relief that excludes network tokens undermines tax simplification and market-structure coherence.

In this context, we are concerned that pending proposals may limit de minimis relief solely to GENIUS-compliant payment stablecoins, under the theory that only these tokens are "cash-like" and therefore suitable for a narrow small-transaction exemption. While we support cash-equivalent treatment for compliant payment stablecoins in everyday contexts, limiting de minimis relief solely to those instruments would undercut the central reason for enacting such a rule: making digital asset payment activity on open networks administratively feasible.

De minimis relief should cover everyday Bitcoin payments made by millions of Americans.

Bitcoin is not used solely as an investment asset; today it also functions as a real-world payment rail. Merchants across the United States—especially small businesses—accept Bitcoin directly or via the Lightning Network to process low-value, high-frequency transactions without the high percentage fees and chargeback risks associated with traditional card networks. Households likewise use Bitcoin for cross-border transfers and remittances, where legacy options can be slow, expensive, or inaccessible.

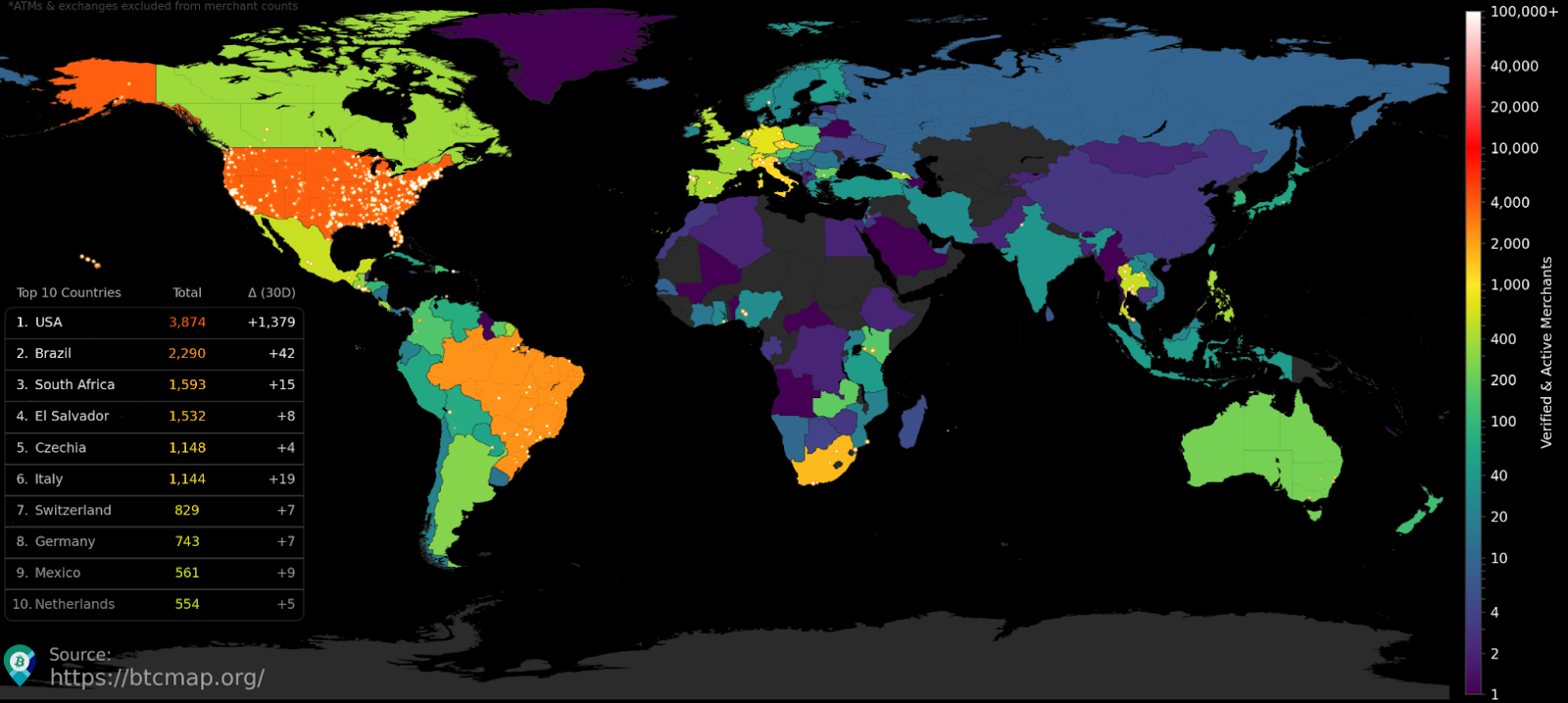

The latest data indicates that the United States is the single largest jurisdiction for Bitcoin payments, with over 3,500 merchants across all 50 states now accepting Bitcoin at the point of sale—more than any other country.³ Today it is estimated that roughly 14% of U.S. adults—approximately 45 million Americans—own cryptocurrency, with Bitcoin by far the most commonly held digital asset.⁴ Federal Reserve survey data likewise suggests that on the order of 7 million Americans used Bitcoin or other network tokens over the course of 2024 to make payments they perceived as faster, cheaper, easier, or more privacy-protective than conventional options.⁵

Current tax treatment, however, treats every small Bitcoin payment as a taxable disposition of property. In theory, a consumer who uses Bitcoin to buy a coffee, tip a delivery driver, or send a small remittance must track cost basis and calculate gain or loss on each transaction, even when the amounts involved are only a few dollars. Extending de minimis relief to qualifying major network tokens would fix this mismatch by aligning tax rules with the policy rationale for de minimis provisions – avoiding disproportionate compliance obligations for everyday, low-value transactions – while preserving full tax recognition for larger, investment-driven disposals.

The network-level reality: Stablecoins also depend on major network tokens.

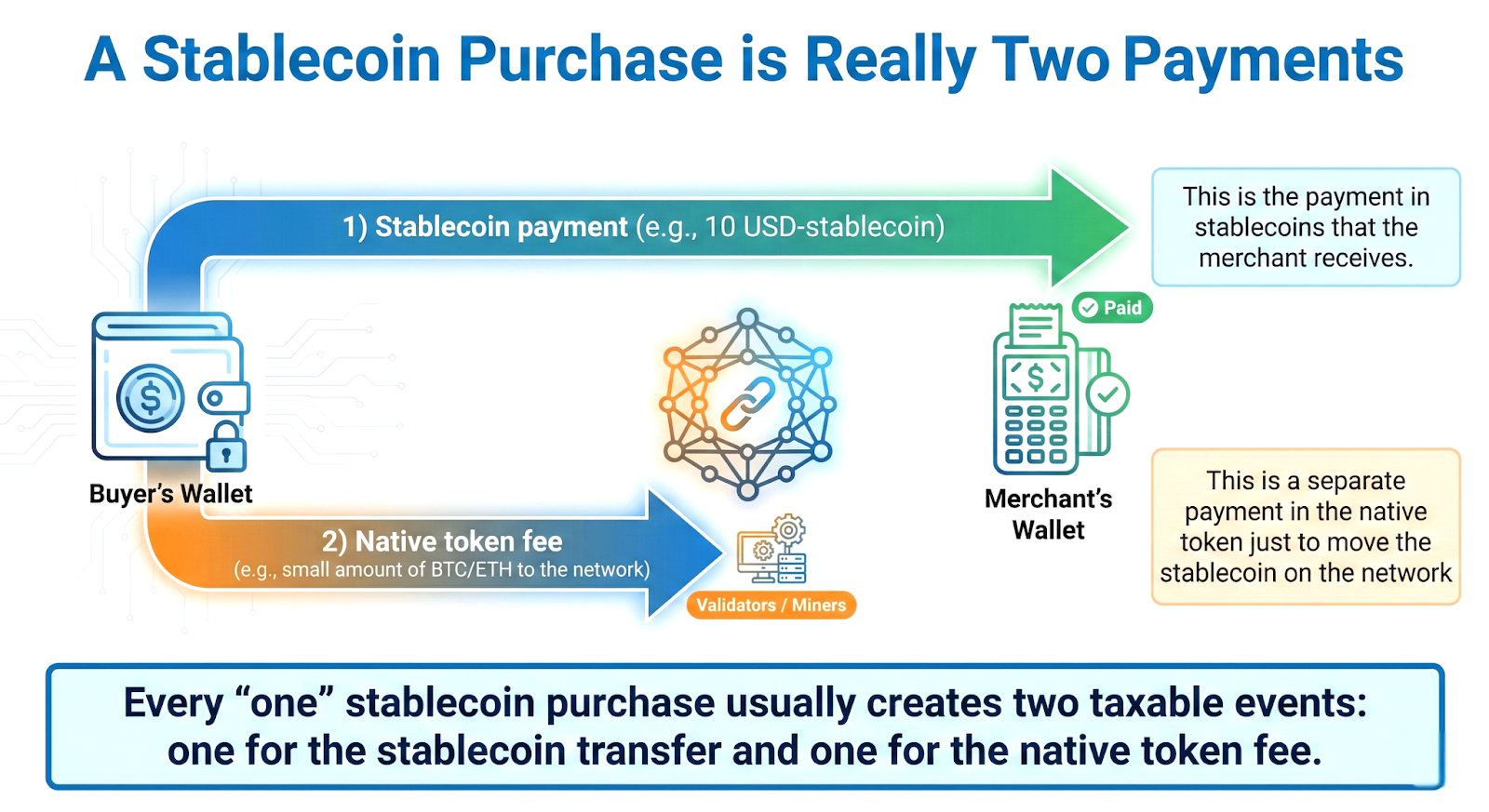

In practice, a payment stablecoin almost never moves independently of the network that carries it. The vast majority of stablecoins circulate on public blockchain networks that rely on a separate network token (such as BTC, ETH, or SOL) for transaction fees and security. When a user sends a payment stablecoin, the transaction typically requires one or more dispositions of that network token to pay network fees ("gas fees"), each of which is currently treated as a taxable event subject to gain or loss recognition and basis tracking.

Below is a diagram that illustrates a standard stablecoin transaction flow:

As illustrated above, even for a purely "dollar-denominated" stablecoin payment, the sender must spend a small amount of the network token to include the transaction on the blockchain. As long as those fee-level dispositions remain fully taxable, users will be forced to track basis and gain/loss on a series of tiny network-token transactions when making routine payments. De minimis relief that ignores the network asset would be akin to exempting the price of a foreign-currency coffee while still requiring taxpayers to calculate and report a gain on foreign credit card processing fees each time they tap their card.

If Congress crafts a de minimis rule that covers only payment stablecoins, but not the network tokens that power their networks, taxpayers and agencies will still face the same core problem: every small payment will entail tracking gains and losses on fee-level network-token transfers, even when the economic value being transferred is denominated in dollars. That outcome would leave the underlying compliance burden largely unmitigated.

Policy Recommendations:

We therefore respectfully recommend pursuing the following policy goals for any digital asset tax package:

1. Cash-like treatment for GENIUS-compliant payment stablecoins

We support a first pillar of reform under which payment stablecoins that meet the GENIUS Act's requirements are treated as cash-like for small-value transactions, subject to no transaction or annual limits, akin to paying with physical cash. GENIUS already defines "payment stablecoin" and imposes rigorous standards around backing, redemption at par, supervision, and disclosures. Incorporating that definition into the tax code would provide clarity and avoid creating an inconsistent or parallel category.

Under this approach, Congress could provide that when a GENIUS-compliant payment stablecoin is used to make payments for goods, services, or peer-to-peer transfers, taxpayers need not recognize gains or losses or engage in burdensome basis tracking that is disproportionate to the economic significance of the transaction. This would be consistent with Congress's expressed aim of allowing dollar-denominated stablecoins to function as a safe, scalable extension of U.S. payment infrastructure and an instrument of dollar competitiveness. Providing tax treatment that reflects their intended use in everyday commerce is therefore a necessary complement to the prudential framework Congress has already enacted.

2. Ensure de minimis relief covers major network tokens

A second pillar is essential if de minimis policy is to work in practice: extending small-transaction relief to major network tokens that meet an objective scale and maturity test. We propose that any network digital asset of a blockchain network with a market capitalization above $25 billion, based on a trailing six-month average using publicly reported market data, be treated as a "qualifying network digital asset" eligible for de minimis treatment on small payments.

Under current and foreseeable market conditions, such a threshold would capture Bitcoin and any other network tokens that achieve sustained, large-cap status and deep liquidity, without opening the door to indiscriminate inclusion of thinly traded or highly speculative assets. It would also give Congress and Treasury a clear, objective line to administer and, if necessary, revisit over time as markets evolve.

3. Adopt value-based accounting with reasonable per-transaction and annual caps

Finally, we urge the Committees to structure any de minimis relief in terms of the dollar amount of the transaction rather than the amount of gain or loss realized. For ordinary households, small merchants, and brokers implementing Form 1099-DA, a transaction-based test is far more administrable and easier to audit than rules keyed to individualized gain calculations. It avoids the inevitable mismatches between broker-reported gains and a taxpayer's own basis records—especially for digital assets acquired before full broker basis reporting is in place, and in situations where taxpayers legitimately use different cost-basis methods than those required of brokers.

Under this approach, Congress could provide that when a qualifying network token is used to pay for goods or services or in a peer-to-peer transfer, the transaction is treated as de minimis – and excluded from both capital gains recognition and information reporting – where (1) the value of the transaction does not exceed a statutory transaction limit (i.e. $600), and (2) the aggregate value of such de minimis transactions does not exceed a statutory annual limit (i.e. $20,000) per taxpayer per year, which would limit the maximum annual capital gain exemption to ~$3,000 per taxpayer. Above these thresholds, ordinary capital gains rules could continue to apply in full, preserving tax recognition for larger, investment-driven disposals.

A transaction-value test has several advantages over gain-based thresholds. It gives taxpayers and brokers a clear, objective rule that can be applied without reconstructing detailed basis histories, particularly for "non-covered" assets acquired before comprehensive broker-basis reporting takes effect. It also avoids confusion arising from differences between broker-calculated gains – often based on FIFO as required by regulation – and the taxpayer's chosen accounting method, which may legitimately rely on specific-lot identification. For the average user buying coffee or groceries, the practical question is whether the payment itself is small, not whether a few dollars of embedded gain or loss happened to accrue.

Interaction with 2026 broker reporting and administrative simplicity

A well-designed de minimis regime for both payment stablecoins and qualifying major network tokens would improve the functioning of the forthcoming Form 1099-DA reporting system. If small-value payments remain fully taxable, brokers and intermediaries will be compelled to report vast numbers of micro-transactions, and taxpayers will face the impossible task of reconciling these reports with their everyday spending.

We would welcome the opportunity to work with your staff on technical refinements to ensure that de minimis tax relief is implemented in a manner consistent with existing Code structure, enforcement practices, the GENIUS Act, and Congress's emerging digital asset market structure framework - so that tax policy reinforces, rather than contradicts, the regulatory clarity Congress is working to deliver. Thank you for your leadership on these issues and for your consideration of these recommendations. We would be pleased to provide additional data, documentation, or testimony as the Committees continue their work on digital asset tax policy.

Respectfully submitted,

Bitcoin Policy Institute

Bitcoin Voter Project

Block

Crypto Council for Innovation

The Digital Chamber

MoonPay

River

ENDNOTES

¹ Responsible Financial Innovation Act of 2025, Discussion Draft (Senate Banking Committee, Sept. 5, 2025) (182 pp.), available at https://www.dwt.com/-/media/files/blogs/financial-services-law-advisor/2025/09/market_structurediscussiondraft9525.pdf

² Jonathan Curry, "IRS Prepping for at Least 8 Billion Crypto Information Returns," Tax Notes (October 25, 2023), https://www.taxnotes.com/featured-news/irs-prepping-least-8-billion-crypto-information-returns/2023/10/25/7hhdp.

³ United States Bitcoin Merchant Dashboard, Btcmap.org, accessed Dec. 22, 2025, data available at https://btcmap.org/country/us/merchants, dashboard available at wickedsmartbitcoin.com/btcmap.

⁴ River Financial, River Bitcoin Adoption Report 2025 (River.com, 2025), available at https://river.com/learn/files/river-bitcoin-adoption-report-2025.pdf.

⁵ Board of Governors of the Federal Reserve System, Economic Well-Being of U.S. Households in 2024, p. 54, available at https://www.federalreserve.gov/publications/files/2024-report-economic-well-being-us-households-202505.pdf.