Who's Been Buying Bitcoin?

This blog post analyzes bitcoin price patterns to show US demand is policy-driven, while foreign demand reflects geopolitical hedging.

This blog post investigates who has been buying bitcoin over the last several months as US policies toward bitcoin have rapidly evolved. The analysis sheds light on bitcoin's role as an investment and as a hedge against geopolitical risk.

This post implements the same method as a recent analysis of international reserve flows and gold prices prior to the 2025 US Presidential Inauguration. In that study, the authors found that the positive returns of gold between April 2024 and January 2025 occurred primarily during non-US business hours, which the authors tentatively attribute to increased demand for gold among foreign investors. However, it was impossible for the authors to distinguish between supply-side and demand-side factors that can both influence the price of gold.

Unlike gold, bitcoin's supply schedule is fixed, so the changes in the price of bitcoin are purely demand-driven. Thus, decomposing bitcoin returns into US and non-US business hours provides insight into which group's demand for bitcoin has been relatively higher or lower.

In this post, I consider US business hours to encompass the interval from 9:00 AM to 8:00 PM Eastern time. I assume that Americans are more likely to purchase or sell bitcoin during this time interval, and foreigners are more likely to do so outside this interval. One potential limitation: the US time interval also includes normal business hours for some other North and South American countries, whose behavior I cannot distinguish from that of investors inside the United States.

Figure 1 illustrates bitcoin's cumulative returns from October 1, 2024 until 10:00 PM Eastern time on November 5, 2024, roughly the time when the winner of the 2024 US Presidential Election became apparent. Foreign investors exhibited steady demand for bitcoin throughout this period.

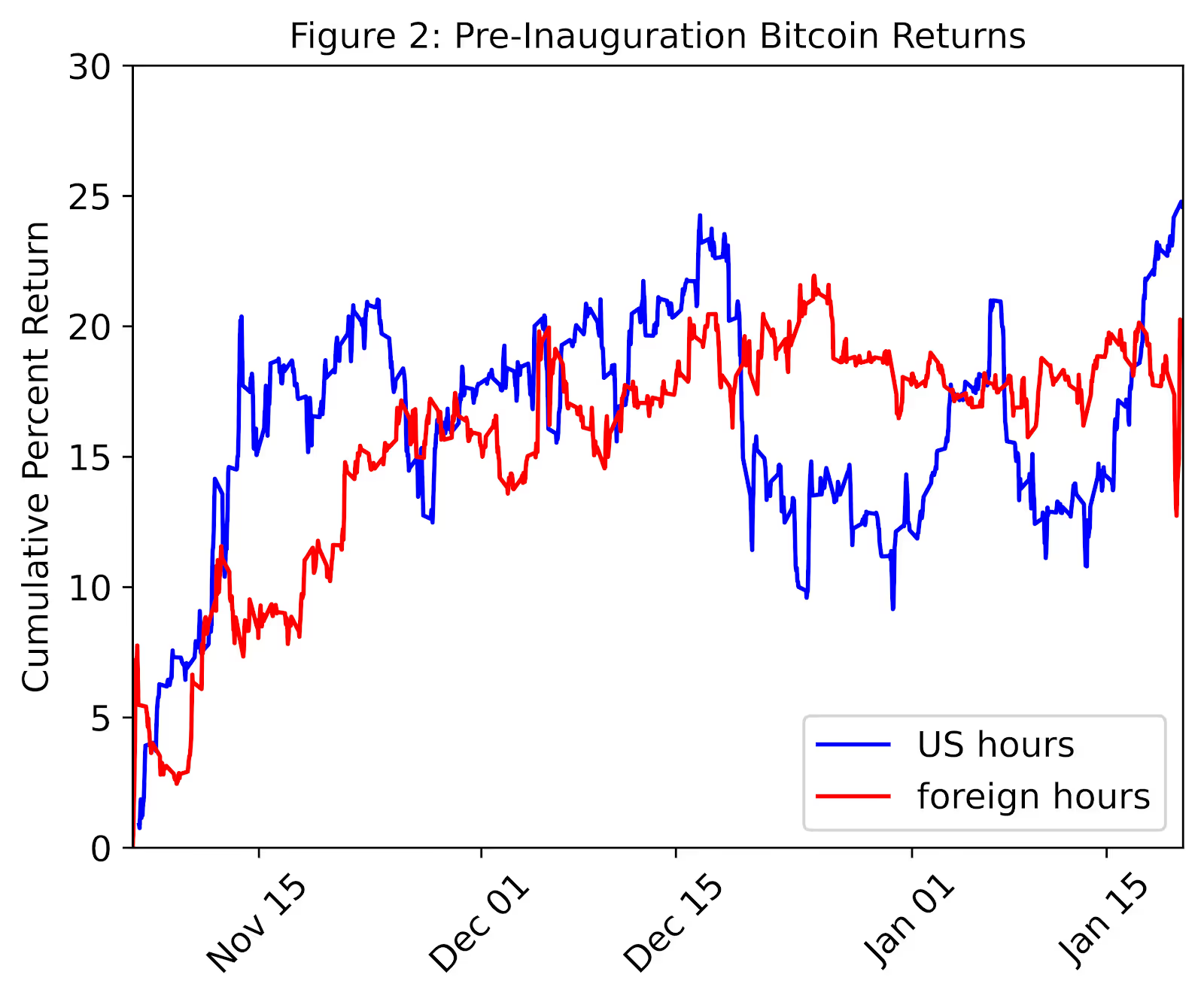

Figure 2 shows bitcoin's total returns from the 2024 US election until 11:00 AM Eastern time on January 20, 2025, one hour before the US Presidential Inauguration. During this transition period, bitcoin appreciated sharply. In the week before the inauguration, US investors had particularly robust demand for bitcoin.

Figure 3 reveals bitcoin's total returns between the US Presidential Inauguration and the signing of the Strategic bitcoin Reserve (SBR) executive order. We see significant bitcoin demand from US investors in the week prior to the executive order.

Lastly, Figure 4 displays bitcoin's cumulative returns between the SBR executive order and the Liberation Day tariffs. Both US and foreign demand for bitcoin declined in the week after the SBR order, while foreign demand picked up in the following weeks.

In summary, this analysis reveals oscillation between US and foreign demand for bitcoin. Foreign demand for bitcoin was strong before the 2024 US election and in the weeks before Liberation Day, while US demand was strong in the week prior to the Inauguration and the week prior to the SBR executive order. This suggests that US demand for bitcoin is relatively more speculative—seeking to profit from shifts in US crypto policy—whereas foreign demand for bitcoin stems from a desire for insurance against geopolitical uncertainty.